Demystifying W-9s: A tax guide for research incentive programs

By Russ Rizzo●6 min. read●Jul 29, 2025

The IRS considers any type of compensation to research participants to be taxable income — whether it’s cash, a cash equivalent (like a gift card, check, or prepaid Visa card), or anything else of monetary value. So it’s important to know the rules.

This article provides an overview of tax requirements for U.S.-based research companies that offer incentives and other rewards to participants.

We’ll break down the tax implications, including:

When and how you need to report payments

What paperwork to file

When you might have to withhold taxes

Potential penalties you could face if you run afoul of the rules

DISCLAIMER: This is not tax advice.

$600 threshold for U.S. participants

For research participants in the U.S., the IRS only requires a payer to report when someone receives $600 or more in a calendar year from the same company. As incentive payments continue to increase, more payees may cross this threshold.

Once you pay a U.S. citizen or permanent resident $600 in a year, you must do two things to keep on the right side of the IRS:

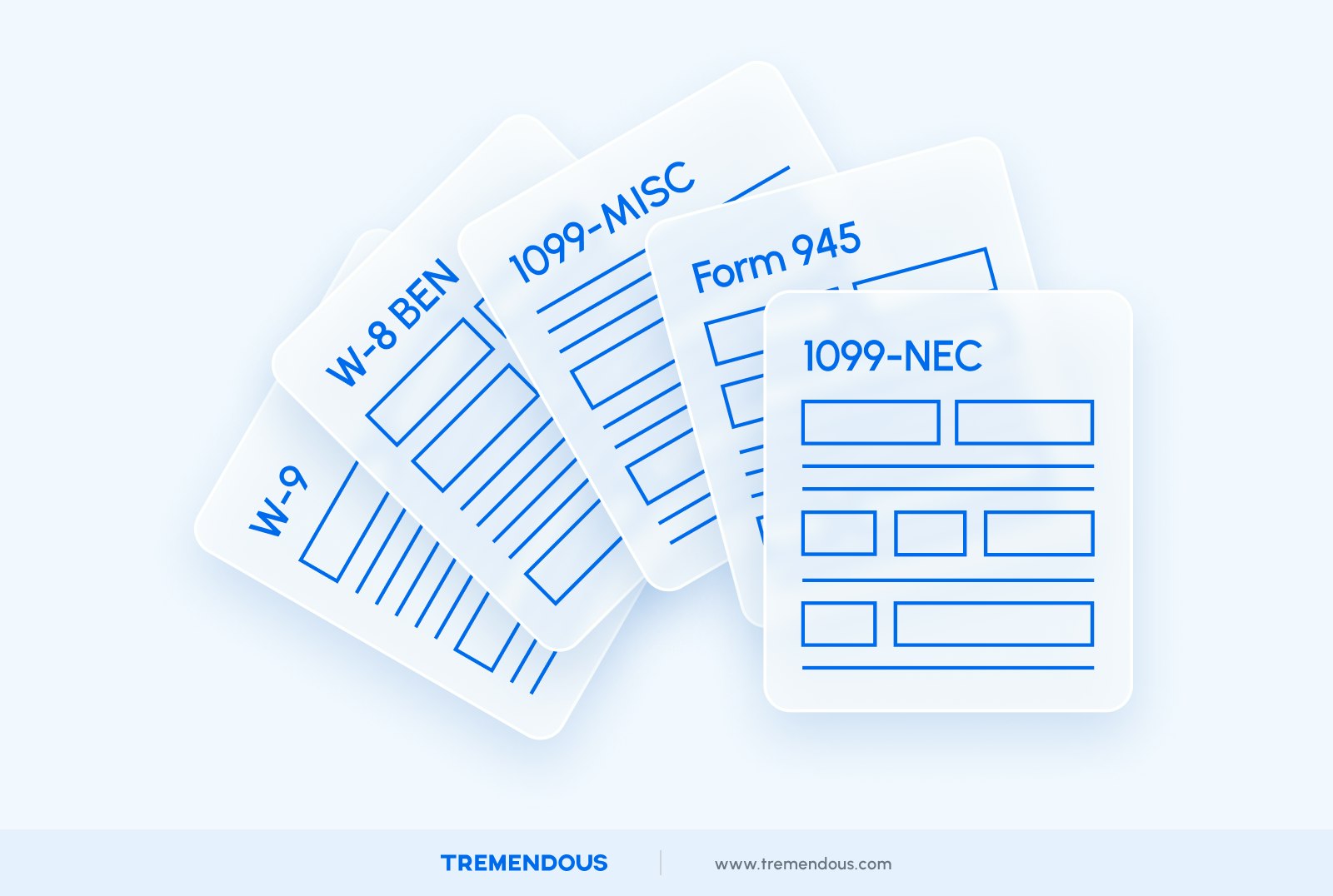

Before tax season, request a W-9 (“Request for Taxpayer Identification Number and Certification”) from the participant. This form will include the person’s (or company’s, if they’re an LLC, for example) tax identification number and/or social security number and other information you’ll need to report their payments when you file taxes.

During tax season, file a 1099-MISC (“Miscellaneous Income”) along with your other tax paperwork, just as you would do for hired freelancers or contract workers.

Companies are not required to withhold taxes from participants in the U.S. They simply report any payments totaling more than $600 in a year to one person.

For U.S. citizens and permanent residents earning less than $600 from one company in a calendar year, there’s no requirement for companies to request a tax form or report payments.

Incentives outside of the U.S.

For participants living outside of the U.S. (“non-resident aliens”), the IRS has stricter reporting and withholding rules.

These rules apply when a participant:

Is a non-citizen

Is not a resident of the U.S.

Does not have a green card

Companies that offer incentives to people outside the U.S. must do the following:

Before tax season, request a W-8 BEN (“Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting”) form from every participant you pay, no matter the amount. (Note: Some universities choose to only collect W-BEN forms for payments over a certain threshold, so this is one potential gray area in the rules.)

Withhold 30% of each payment for taxes. This amount varies depending on the participant’s country and tax status.

Come tax season, report all payments to the IRS using 1042-S (“Foreign Person's U.S. Source Income Subject to Withholding”) and report all tax withholdings on Form 945 (“Annual Return of Withheld Federal Income Tax”).

Tracking payments

Research institutions issue their own guidelines for the type of information researchers should collect at the beginning of a study (examples: University of Dayton, Vanderbilt University, University of Vermont, University of Virginia).

When researchers anticipate making several payments to the same U.S.-based participant over the course of a year, they’ll typically request a W-9 tax form at the start of the study. Others might wait until they’ve reached the $600 threshold.

On the other hand, if it’s unlikely a participant will reach the threshold, some organizations advise against requesting unnecessary personal information.

For participants outside the U.S., IRS rules call for researchers to collect tax forms on everyone, no matter the payment amount. So it’s important to track everything. (Note: In practice, some organizations establish their own procedures for what information and forms to request, depending on the payment amount).

Failure to collect

The IRS requires companies to make “solicitations” at the start of the business relationship and before the end of each year — and document these for proof, in case the recipient fails to provide a W-9 or W-8 BEN.

If someone in the U.S. fails to submit a W-9 form, you’re required to make a “backup withholding” of 24% of their payments and report that on Form 945. The participant can also be fined $50.

If you make a payment to someone in the U.S. and miss filing a 1099-MISC, you could face penalties between $60 and $330 per form.

If you make a payment to someone outside of the U.S. without collecting a W-8 BEN, you could be subject to a fine of up to 30% of the payment, plus interest and penalties. There are steeper penalties if the IRS finds that you intentionally disregarded requirements.

Accurate, timely research is central to many companies’ ability to grow and innovate. By sticking to these rules, you can get the data you need while reducing your risk of running afoul of the Tax Man.

Disclaimer: This overview is meant to give you the lay of the land, not replace a proper map. It pulls together key themes and pitfalls we see around reward-related taxes, but it doesn’t cover every twist in the code—or your company’s unique facts. Before you rely on anything here, run it past your own tax advisors to be sure you’re handling rewards in a way that’s fully compliant and optimized for your situation